Looking for a Las Vegas house? Lack of supply may be a problem

With the spring buying season underway, Las Vegas house hunters may have to spend more time scrolling through listings and visiting properties — and pay more than they hoped.

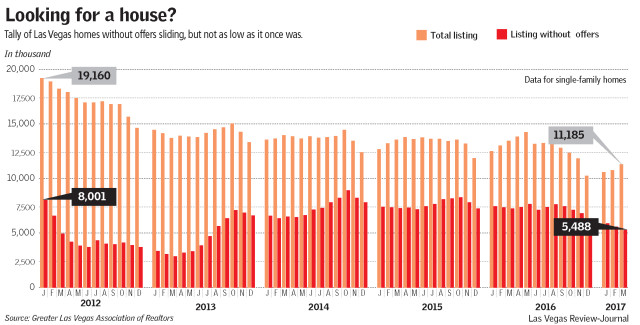

Southern Nevada’s inventory of available homes has been sliding for months amid a nationwide drop. Sales totals are still climbing, and the menu of options is not so diminshed that it’s impossible to find a place, but availability has reached its lowest point since summer 2013.

A shrinking supply can be good for sellers, who can fetch higher prices amid strong demand and decreased competition. But it doesn’t bode well for buyers or for real estate agents, who have fewer properties to sell.

Roughly 11,200 single-family homes were listed for sale in Southern Nevada at the end of March, down 17 percent from a year earlier. Within that, almost 5,500 listings did not have offers, down 24 percent from a year earlier and the seventh consecutive monthly slide, according to figures from the Greater Las Vegas Association of Realtors, which pulls data from its resale-heavy listing service.

Buyers “are aplenty,” 1st Realty Group owner Thomas Blanchard said, but “we just don’t have the properties to sell them.”

Homes worth ‘top dollar?’

Factors pushing or holding availability down include increased demand from buyers, a still-large tally of underwater borrowers who can’t easily sell, and a sizable number of rental homes that aren’t listed for sale.

Nationally, inventory has dropped in part because rising prices have made it “increasingly difficult” for homeowners to buy a place after they sell, according to Cheryl Young, a senior economist with listing service Trulia. Not only are “buyers in the hottest markets likely to be priced out,” but sellers “may be locked in to their existing homes.”

If that’s a factor in Las Vegas, it’s almost surely not as acute as in cities where home values have reached new peaks.

The median sales price of previously owned single-family homes — the bulk of Southern Nevada’s market — was $242,000 last month. That’s more than double the market’s low point but still below its peak of $315,000 in 2006, during the housing bubble, GLVAR data show.

A poster child for the real estate boom and bust, Las Vegas was one of the hardest hit markets in the country during the recession, and its economy, despite having improved, still lags behind most cities in some ways. By comparison, home prices in 89 metro areas hit record highs last year, according to housing tracker Attom Data Solutions.

Still, the pace of sales has gained speed locally, with demand fueled by the rising population, job growth and higher wages, according to Brian Gordon, co-owner of Las Vegas research and consulting firm Applied Analysis.

Almost 47,000 previously owned homes were sold in the Las Vegas Valley last year, up 6.6 percent from 2015, according to the company’s residential research arm, SalesTraq.

When homeowners hear it’s a seller’s market, they “instinctively feel” their property is worth “top dollar,” Re/Max Excellence Realty agent Tim Kelly Kiernan said.

As he sees it, many homes are overpriced today, and if properties were priced at fair market value, sales totals “would be even greater.”

Still drowning

Meanwhile, two ongoing issues are crimping the supply of listings, some real estate pros said.

Upside-down homeowners, whose mortgage outweighs their home’s value, can sell only with bank approval. The valley’s share of such borrowers has plunged in recent years, but Las Vegas remains the underwater capital of America.

An estimated 16.6 percent of local borrowers were upside-down in the fourth quarter, down from 71 percent in early 2012 but still highest among large metro areas, according to listing service Zillow.

Trulia’s Young noted that in cities where “home values have been slow to recover,” borrowers are unable to sell because they’re still upside-down.

On top of that, investors took many homes off the for-sale market when they bought cheap houses by the dozen after the economy tanked and turned them into rentals.

Their buying binge helped revive the market, but there are few, if any, signs that the biggest investors are selling.

“Those homes should be on the market today, and they’re not,” said Blanchard of 1st Realty.

The sliding inventory also means that people who sell houses may have fewer to offer.

GLVAR President David J. Tina, co-owner of Urban Nest Realty, said higher prices produce bigger commissions, which can help real estate agents offset a drop in sales totals.

But as Scott Beaudry, owner of Better Homes and Gardens Real Estate Universal, noted, if there are no cans of soup to buy, there are no cans of soup to sell.

Contact Eli Segall at esegall@reviewjournal.com or 702-383-0342. Follow @eli_segall on Twitter.

Las Vegas houses: Listings down, sales and prices up

5,488: Single-family homes listed without offers in March, down 24 percent from year earlier

$242,000: Median sales price of single-family homes in March, up 10 percent from year earlier

3,195: Single-family homes sold in March, up 15 percent from year earlier

Related

Inventory for home buyers across US at 20-year low

Las Vegas home prices up from year ago, but inventory still tight

Experts say demand for custom home lots increases